Wise Business Account: review 2026

Last updated: 30.06.2026

Contents

Summary

Wise Business is a multi-currency account with no monthly fee. The Advanced plan (one-off £50 setup) unlocks receiving payments in 22 currencies at the mid-market FX rate. Not a bank — safeguarding applies, not FSCS.Pros

- Mid-market FX rate on international payments in 40+ currencies with transparent, low fees

- Local account details in multiple currencies (GBP, EUR, USD and more), letting overseas clients pay as if locally

- Cashback on eligible Visa debit card spending

- Direct integrations with Xero, QuickBooks and other accounting platforms

- Virtual cards included, with Apple Pay and Google Pay support

Cons

- No FSCS protection

- no telephone support

- £50 one-off setup fee for the Advanced plan required to receive payments

- no overdraft or lending products.

Key facts

| Monthly fee | 0,00 £ |

| Debit card | ✓ |

| Credit card | ✗ |

| Virtual credit cards | ✓ |

| Free cash withdrawal | ✗ |

| Number of sub-accounts | – |

| Online banking users | – |

| Electronic transfers | ✓ |

| Apple Pay | ✓ |

| Google Pay | ✓ |

| 3D Secure for online payments | ✓ |

| Deposit protection | ✗ |

| Rating | 4.0 /5 |

Strengths in detail

How well the provider covers the most important areas.

A closer look

What the Wise Business Account is and who it suits

Wise Business is a multi-currency business account built around one central proposition: letting UK companies pay and receive money internationally at the mid-market exchange rate, with no hidden markup folded into the rate. It’s offered by Wise Payments Limited, an electronic money institution (EMI) authorised and regulated by the Financial Conduct Authority. The UK IBAN uses the GB prefix, and the registered office sits in London.

The account works best for small and medium-sized businesses dealing in more than one currency regularly. Freelancers billing clients in the US, Germany or Australia; e-commerce sellers receiving payouts from Shopify, Amazon or Etsy in local currencies; agencies paying contractors across borders. In testing, onboarding for a sole-trader structure took under 20 minutes and local USD and EUR account details were available immediately after verification. It’s quick, and it’s straightforward. Most structures are through and approved the same day.

It’s a poor fit for businesses that need a lending relationship, an overdraft buffer, or a dedicated relationship manager. It’s also not suited to businesses whose transactions are entirely domestic and in pounds sterling, because in that scenario the main advantage disappears and you’re left with a capable but not especially differentiated current account. Brick-and-mortar businesses that handle significant cash volumes will find no coin or note deposit facility here.

Wise isn’t a bank. That single fact shapes everything else in this review: the fee model, the protection structure, and the use-case ceiling. There’s no getting around it, and it’s worth knowing upfront.

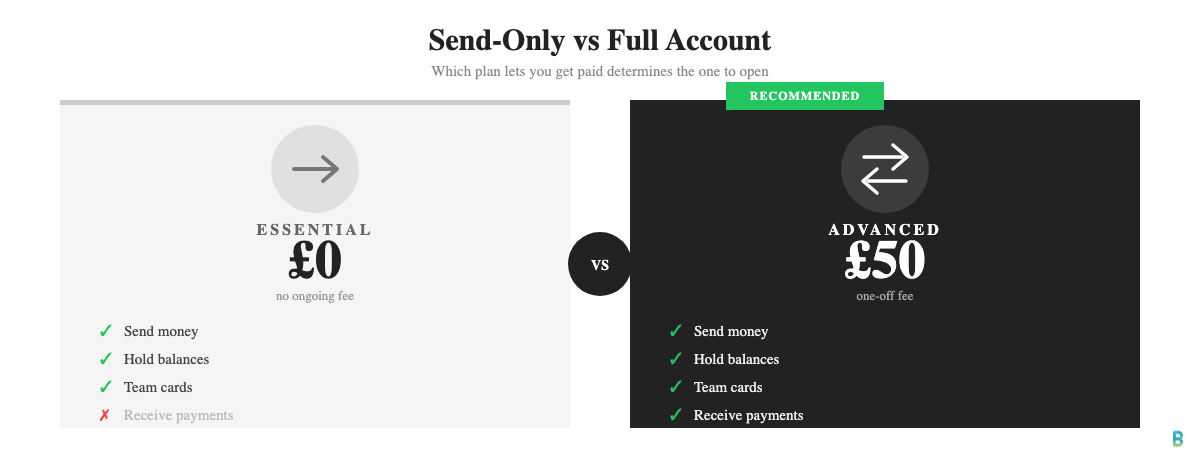

Essential vs Advanced: the two-tier plan structure

Wise Business uses a two-plan structure that catches many applicants off guard. Understanding the difference before you apply avoids a frustrating discovery at the point when you need to get paid.

The Essential plan is free to open. It lets you hold balances in multiple currencies, send money internationally, and issue debit cards to your team. What it doesn’t do is let you receive incoming payments or set up direct debits. That means no GBP sort code and account number to share with UK clients, no EUR IBAN for European customers, and no ability to collect subscriptions by direct debit. For a business that needs to get paid, it’s outright unusable without the upgrade.

The Advanced plan costs a one-off £50 fee, charged once at account setup. After that, there’s no monthly charge. The Advanced plan unlocks local account details in 22 currencies, the ability to receive payments from overseas clients, direct debit setup, invoice generation, payment links and QR codes. For any business that needs to be paid, the Advanced plan is clearly the one to open. Most UK businesses will pay the £50 fee from day one, and that’s fine. It’s a one-time charge.

- Essential: £0, no ongoing fee; send-only; no incoming payments

- Advanced: £50 one-off fee; full incoming payments in 22 currencies; direct debits; invoice tools

The fee structure is otherwise identical across both plans. You pay per transaction, not per month, which gives the account a genuinely low cost floor for businesses that don’t transact heavily in foreign currency every week. Beyond that one-time fee, you’re not paying anything to hold the account.

Real costs in detail: fees, FX rates and what you’ll actually pay

The ongoing monthly maintenance fee is £0. This contrasts with many traditional UK business accounts that charge £5 to £12.50 per month as a base fee before any transactions. The one-off £50 Advanced plan fee is the only fixed cost you pay to open the account.

Foreign exchange conversion uses the mid-market rate with a disclosed percentage fee added at the point of confirmation. For GBP to EUR, the fee sits at around 0.37% based on current published rates. Converting £5,000 to euros costs roughly £18.50 in fees at that rate. A high-street bank embedding a 2% margin in its published rate would cost £100 for the same conversion. That’s the difference.

For other currency pairs, the percentage rises as the pair becomes less liquid. Major pairs such as GBP/USD or EUR/USD sit below 0.5% in most cases. More exotic pairs can reach 1 to 2%, which is still materially cheaper than bank spreads but worth checking before a large conversion. All fees are shown before you confirm, so there’s no surprise at the other end.

ATM withdrawals aren’t free beyond a monthly allowance. Wise provides two free withdrawals per month up to a combined limit of £200. After that, a fee of 1.75% applies plus a flat £0.50 charge per withdrawal. Sending money between Wise accounts is free. Receiving money into your local currency accounts is generally free; receiving a SWIFT wire may carry a small incoming fee depending on the intermediary banks involved.

For businesses sending more than £20,000 a month in foreign currency, Wise offers volume discounts. The percentage fee decreases at higher monthly volumes, which makes the account increasingly competitive for businesses with material international payment flows.

Multi-currency accounts and international payments

The core practical advantage of the Wise Business account is the multi-currency setup. Once you’re on the Advanced plan, you receive local account details in up to 22 currencies, including GBP, EUR, USD, AUD and SGD. An overseas client can pay you as if they were paying a local bank in their own country, with no cross-border wire required on their side. That’s genuinely useful when you’re billing internationally at scale.

Sending money goes to 70 or more countries. Wise reports that 70% of transfers arrive in 20 seconds and 95% within 24 hours for the main corridors. That’s genuinely fast. GBP-to-EUR and GBP-to-USD same-day arrivals are the norm for standard banking hours. More remote corridors or payments involving intermediate banks can take one to two business days.

The account supports batch payments via CSV file upload, useful for businesses running payroll across multiple currencies or paying large numbers of freelancers each month. The batch tool handles up to 1,000 recipients in a single upload. Payments run from the relevant currency balance in your account, so you can pre-fund a EUR balance and run a batch of EUR payroll without converting on the day.

The account also lets you hold balances and earn a return on GBP, EUR and USD holdings. It’s not the same as a savings account and the returns aren’t guaranteed, but for businesses sitting on large currency balances it’s a useful feature most business current accounts don’t offer.

Cards, expense management and digital wallets

Every Wise Business account holder can order a physical business debit card, issued on the Visa network. There’s no credit card option. Wise doesn’t extend credit; that’s a deliberate structural decision rather than an oversight, and it shapes the risk profile of the account in a way that matters for businesses used to working with an overdraft buffer.

Virtual cards can be generated immediately inside the app. Adding a virtual card takes under a minute, and in testing it appeared in the Apple Pay wallet within two minutes. Google Pay’s fully supported too. Contactless payments from a phone or watch work from day one without waiting for a physical card to arrive.

3D Secure authentication is active on all online card payments. Spending limits can be adjusted through the app, and individual cards issued to team members can have their own separate limits. This makes it straightforward to give employees a card with a defined monthly budget without needing to issue a full account-level card.

Wise currently offers cashback on eligible card spending. The cashback rate and eligible categories are shown in the app and vary, but it represents a meaningful benefit for businesses with high card spend, particularly on international transactions where competitors often charge FX fees that Wise avoids by converting at the real rate.

Team access, permissions and batch payments

Wise Business supports multiple users on a single account, which is a real operational benefit for businesses with finance teams or multiple payment approvers. The permission structure gives each user a defined role: view-only users can see balances and transactions; payers can initiate and confirm payments; admins can manage the account and add or remove team members.

In practice, that means giving a bookkeeper read access without giving them payment rights, and separating payment initiation from approval for businesses that run a two-person process on larger transfers. It’s a setup that’s genuinely practical for small teams.

The batch payment tool supports up to 1,000 recipients per upload and is compatible with CSV formats from Xero, QuickBooks and most payroll software. For businesses paying the same set of contractors or suppliers each month, the batch upload cuts what would otherwise be an hour of manual transfers down to a few minutes of file preparation and review.

Accounting integrations and business tools

Wise connects natively with Xero, QuickBooks and FreeAgent, pushing transaction data automatically so bookkeepers don’t need to export spreadsheets. The integration’s read-only from the accounting software side; Wise pushes the data, the accounting software categorises and reconciles it. It’s one of the stronger practical differentiators from simpler EMI accounts that only offer CSV downloads. That’s not a small thing if you’re reconciling across currencies.

The built-in invoicing tool is straightforward rather than comprehensive. It handles client name, line items, due date and bank details. For businesses that need recurring invoices, credit notes, multi-currency invoice templates or client payment portals, a dedicated invoicing platform is still the better choice. For straightforward one-off billing, the tool works without a third-party subscription.

API access is available for businesses that want to automate payment initiation, reconciliation or reporting from their own systems. This is relevant for e-commerce businesses connecting Wise to their checkout or order-management stack, and for SaaS companies paying international subscriptions or commissions at scale.

How to open a Wise Business Account step by step

The application’s entirely online. There’s no branch to visit, no telephone call required and no paper form to post. You start at the Wise website or download the Wise app. Registration asks for a business email address and password, followed by questions about business structure, nature of trading, expected transaction volumes and countries you send money to.

Identity verification uses automated document scanning. For a sole trader or director of a small limited company, you upload a passport or driving licence and complete a short video selfie for liveness detection. UK limited companies need their Companies House registration number; Wise cross-references that automatically, so you don’t need to upload a certificate of incorporation separately. Most applications are approved within a few hours for straightforward structures. It’s a fast process when you’ve got all your details to hand.

More complex structures take longer. Businesses with multiple beneficial owners, trusts, or companies in sectors Wise classifies as higher risk (financial services, gambling, certain legal services) may take one to three business days or may be declined. Once approved, GBP local account details are issued immediately. Adding EUR, USD or other currency accounts is a one-click action in the dashboard.

App, web platform and customer support

The Wise mobile app is available on iOS and Android. It rates 4.8 out of 5 on Google Play based on nearly two million ratings, and 4.3 out of 5 on Trustpilot based on almost 294,000 reviews as of June 2026. The interface separates personal and business accounts cleanly if you hold both. The business dashboard shows balances by currency, a real-time transaction feed, pending transfers, and a team management panel.

The web platform carries the same features as the mobile app, including batch payments, invoicing, and accounting integrations. There’s no functionality gap between mobile and desktop; both routes work for day-to-day account management.

Customer support operates through in-app chat and email. There’s no telephone support line, which is a recurring source of frustration for users who face an urgent issue such as a blocked card abroad or a delayed transfer. Response times on chat during UK business hours are generally under two hours for simple queries. Complex disputes, particularly those involving account holds or compliance reviews, can take several days to resolve by email. No dedicated account manager is assigned to individual business accounts.

What customers actually say

Recurring praise across independent review platforms centres on three themes: the transparency of fees before you confirm a payment, the speed of international transfers for major corridors, and the simplicity of managing multiple currency balances in a single dashboard. Business users frequently cite the Xero and QuickBooks integrations and the batch payment tool as genuine time savers. The positive reviews are consistent and the sentiment holds across tens of thousands of verified business accounts.

Recurring complaints follow a consistent pattern. The most common negative theme is customer support, specifically the absence of telephone support and inconsistent resolution speed for account holds or compliance-triggered queries. A second recurring complaint involves verification delays for businesses with complex ownership structures or for newer businesses without a long trading history. A smaller cluster of negative reviews relates to accounts being suspended during periodic compliance reviews with limited communication from Wise about the timeline for reinstatement.

This last pattern isn’t unique to Wise. It reflects a sector-wide approach among FCA-regulated EMIs that use automated compliance monitoring. The practical risk is higher for businesses that use Wise as their sole transactional account; businesses that keep a primary bank account open alongside Wise are less exposed to an operational disruption if Wise’s compliance process flags an account for review.

How your money is protected: FSCS, safeguarding and regulation

Wise Payments Limited is authorised and regulated by the Financial Conduct Authority as an electronic money institution. It’s not a bank. This distinction has a direct consequence for how your money is protected.

The Financial Services Compensation Scheme covers deposits up to £85,000 per eligible claimant at authorised banks and building societies. Wise operates under a different protection model called safeguarding. Under FCA e-money rules, Wise is required to hold client funds separately from its own operating money in ring-fenced accounts at regulated banks or in qualifying liquid assets. If Wise became insolvent, the ring-fenced funds would be returned to customers in priority over other creditors.

Safeguarding provides meaningful protection. The structural difference is this: FSCS coverage is a statutory guarantee backed by a government-administered fund, while safeguarding depends on the correct administration of the ring-fence by the EMI itself. For most small businesses holding a working capital balance, the practical risk difference is modest. It’s not nothing, but it’s not alarming either. For businesses holding very large balances, it’s worth understanding before choosing Wise as a primary account.

Wise publishes its safeguarding reports publicly. The FCA register entry for Wise Payments Limited can be verified directly on the FCA website. Security features on the account include multi-factor authentication, biometric login, real-time transaction alerts and 3D Secure on card payments.

Wise vs alternatives: Airwallex, Revolut Business and Tide

Three alternatives come up most often when UK businesses are comparing Wise: Airwallex, Revolut Business and Tide. Each is meaningfully different in pricing model and use-case fit.

Airwallex targets businesses with heavier multi-currency payment volumes and more complex treasury needs. It offers interbank FX rates with a 0.5% margin on major pairs and no setup fee. The platform’s API capabilities are stronger, and it’s better suited to businesses that need to automate payment flows or run multi-entity accounting. The trade-off is a more complex onboarding and a platform that’s harder to use for occasional international payments.

Revolut Business operates a monthly subscription model with a free plan and paid tiers from £19 to £79 per month. Revolut received a UK banking licence in March 2026, which means balances on eligible accounts will eventually carry FSCS protection, a significant regulatory advantage over Wise. The FX fee structure on Revolut’s paid plans includes fair usage limits, however, and the platform’s customer support has received similar complaints to Wise about slow resolution for account holds.

Tide is a UK-focused business account built for domestic SMEs rather than international payments. It offers a free plan with a monthly fee option for extra features. Tide charges 20p per bank transfer, which makes it more expensive than Wise for businesses with high domestic transfer volumes, but more straightforward for businesses that primarily operate in pounds and need a solid UK current account rather than multi-currency capability.

The simplest framework: use Wise when international payments are a regular need and FX transparency matters; use Revolut when you want a banking-licensed product with subscription-based pricing; use Tide when your operations are primarily domestic and you want a no-frills UK business current account.

Verdict: who should open a Wise Business Account

Wise Business earns a strong recommendation for any UK business that sends or receives money internationally on a regular basis. The mid-market exchange rate, the transparent fee-before-confirmation model, and the multi-currency local account details (via the Advanced plan) represent genuine savings over a traditional business bank account for this use case. The absence of a monthly fee, combined with robust accounting integrations and the batch payment tool, makes the total cost of ownership competitive even after the one-off £50 Advanced plan fee.

It’s not the right primary choice for businesses that need an overdraft, a lending product or FSCS protection on significant balances. It’s also not ideal for businesses that prioritise telephone customer support or that anticipate needing a dedicated relationship manager during periods of growth. For those businesses, a fully licensed UK bank such as Starling or one of the high-street names will provide protections and services that Wise structurally can’t.

Used alongside a primary UK bank account, Wise works exceptionally well as a foreign-payments layer. Used as a standalone account by a domestic-only business, it offers less differentiation. The rating reflects a genuinely strong product for a specific type of customer rather than a universal recommendation.

How safe is Wise Business Account?

Wise Business Account vs alternatives

A direct comparison of the key conditions against the strongest competitors in the market.

Wise Business AccountReviewed Wise Business AccountReviewed | Starling Business Account | Mettle Business Account | Revolut Business Account | |

| Rating | 4.0 /5 | 5.0 /5 | 4.0 /5 | 4.0 /5 |

| Monthly fee | 0,00 £ | 0,00 £ | 0,00 £ | 10,00 £ |

| Debit card | ✓ | ✓ | ✓ | ✓ |

| Credit card | ✗ | ✗ | ✗ | ✗ |

| Virtual credit cards | ✓ | ✗ | ✗ | ✓ |

| Free cash withdrawal | ✗ | ✓ | ✗ | ✗ |

| Number of sub-accounts | – | – | – | – |

| Online banking users | – | – | – | – |

| Electronic transfers | ✓ | ✓ | ✓ | ✓ |

| Apple Pay | ✓ | ✓ | ✓ | ✓ |

| Google Pay | ✓ | ✓ | ✓ | ✓ |

| 3D Secure for online payments | ✓ | ✓ | ✓ | ✓ |

| Deposit protection | ✗ | 85.000 | ✗ | 120.000 |

How we rate

More comparisons

About the author

Frequently asked questions

Wise Business Account is open to UK-registered sole traders, limited companies, partnerships and other business types. You need a UK address and valid ID. Some high-risk business categories (e.g. financial services, gambling) may be declined at Wise's discretion.

The ongoing monthly fee is 0.00 GBP. Wise charges a one-off setup fee when you first open the account. Currency conversion and some international transfers carry per-transaction fees based on a small percentage above the mid-market rate.

No. Wise is an FCA-authorised electronic money institution, not a bank, so the FSCS 120,000 GBP per person per bank guarantee does not apply. Wise safeguards customer funds in segregated accounts at regulated banks and government bonds under FCA e-money rules, which is a different but still regulated form of protection.

Go to wise.com/gb/business and register with your company details and Companies House number (for Ltd companies) or personal details (for sole traders). Complete identity verification via the app using a selfie and document scan. Most applicants receive a decision the same day and the one-off setup fee is charged at that point.

Wise is regulated by the FCA and uses multi-factor authentication, biometric login, real-time transaction alerts and 3D Secure on card payments. Customer funds are held in segregated accounts separate from Wise's own money. The main caveat is the absence of FSCS coverage compared with a fully licensed UK bank.

For most UK limited companies, interest or gains earned on foreign currency balances held in a business account are subject to corporation tax, not the Personal Savings Allowance (which applies to individuals). Sole traders report business income and any interest under self-assessment. Tax treatment depends on your business structure; consult an accountant for advice specific to your situation.