Kroo Current Account: review 2026

Last updated: 13.06.2026

Contents

Summary

Kroo is a fully licensed UK bank that pays credit interest on its current account balance, charges nothing for everyday spending or overseas ATM withdrawals, and is covered by the FSCS up to 120,000 GBP per person. In our test it suits people who want a genuinely free account that earns a little interest, but those needing branch access or a broad product range will find it limited. It scores 80 out of 100 in our rating, earning 4 out of 5 stars.

Pros

- Credit interest paid directly on the current account balance, no conditions attached

- No monthly fee and no charges for overseas card spending or ATM withdrawals abroad

- Fully licensed UK bank, deposits protected by the FSCS up to 120,000 GBP per person per bank

- Apple Pay and Google Pay supported from day one

- Clean, straightforward app available on iOS and Android

Cons

- App-only with no branches or phone banking

- Newer, smaller bank with a narrower product range than established names

- Interest rate on the account balance is variable and subject to change

- No credit card option available

Key facts

| Monthly fee | £0/month |

| Debit card | ✓ |

| Credit card | ✗ |

| Apple Pay | ✓ |

| Google Pay | ✓ |

| Cash withdrawal abroad | Free (no Kroo fees) |

| Online account opening | ✓ |

| Deposit protection | 85.000 |

| iOS app | ✓ |

| Branches | ✗ |

| Rating | 4.0 /5 |

Strengths in detail

How well the provider covers the most important areas.

A closer look

What Kroo is and who it suits best

Kroo is a fully licensed UK bank, not a fintech operating on someone else’s banking licence. That distinction matters more than it sounds. The bank holds its own authorisation from the Financial Conduct Authority, which means it can take deposits in its own right and pass on FSCS protection up to £85,000 per eligible depositor. For a bank that launched its full current account only in 2023, that regulatory standing gives it genuine credibility.

The account is aimed squarely at people who live on their phone and travel regularly. There are no branches. There is no phone number you can call and wait on hold for forty minutes. If that sounds like a dealbreaker, Kroo is not for you. Equally, if you rely on paying in cash, need a connected savings account with a competitive fixed rate, or want an overdraft facility backed by years of relationship history, look at an established high-street bank. Kroo currently has a limited product range. It does one thing at a time, and for now that one thing is a zero-fee, interest-bearing current account.

The people who genuinely benefit are frequent travellers, younger professionals fed up with the big banks, and anyone whose frustration with legacy banking apps has reached a tipping point. Kroo also suits those who habitually keep a meaningful balance in their current account, because earning interest on everyday balances is still unusual among UK current accounts.

Costs, fees and what you actually pay

The headline figure is £0 per month. No monthly fee, no premium tier required to unlock the basics. In our test, we went through the entire sign-up and first month of use without encountering a single mandatory charge. That zero-fee structure extends to the things that typically catch people out with challenger accounts.

Spending abroad with the Kroo debit card attracts no foreign transaction fee. Kroo uses Mastercard’s own exchange rate, which is one of the tightest available, with no added percentage on top. ATM withdrawals overseas are free of any Kroo charge, though the ATM operator itself may impose its own fee. For frequent travellers, the saving relative to a standard UK current account can comfortably run to several pounds per trip.

- Monthly account fee: £0

- UK debit card transactions: free

- Foreign currency spending: no Kroo fee, Mastercard rate applied

- ATM withdrawals abroad: free (subject to operator charges)

- Instant bank transfers (Faster Payments): free

- No credit card product available

There is no tiered pricing here. Kroo does not have a standard account and a premium account. Every customer gets the same terms. That simplicity is deliberate, and it is worth noting: if you are comparing Kroo against a bank that advertises a fee but bundles in travel insurance, you need to assess whether you actually use those extras. For a traveller who already has a good travel insurance policy, Kroo’s free foreign spending is arguably the better deal.

The Kroo debit card: payments and limits

Kroo issues a Mastercard debit card. Mastercard’s global acceptance network is the second-largest in the world, so the card works reliably in the UK, across the EU and in most markets further afield. There is no Visa option, and there is no credit card. If your hotel or car rental company requires a credit card for a deposit hold, you will need a separate card for that purpose.

Apple Pay and Google Pay are both supported. In our test, the card was added to both wallets within a few minutes of the account opening, which matters for anyone who rarely carries a physical card. Contactless payments via the phone worked without issue across multiple retailers.

Virtual card functionality is not a prominently advertised feature. Kroo’s focus is on the physical card and the wallet integrations rather than disposable virtual cards for online subscriptions. The app does allow you to freeze and unfreeze your card instantly, which provides a practical substitute for security-conscious online spending. Payment limits are set within the app, and customer support can adjust them on request, though the bank’s in-app messaging function handles most of these interactions rather than a phone line.

Opening the account: steps, identity checks and your IBAN

The application is entirely app-based. There is no desktop web application for account opening, which follows the same logic as Monzo and Starling. You download the Kroo app from the App Store or Google Play, enter your mobile number, and work through the identity verification process.

Identity verification uses a photo ID scan combined with a live selfie check. Accepted documents include a UK passport, a UK driving licence, or a qualifying non-UK passport. The process is powered by a third-party identity verification provider running automated checks, so the result is typically near-instant during normal hours. In our test, the full process from downloading the app to a confirmed open account took under ten minutes, which is competitive even by challenger bank standards.

Once the account is open, Kroo issues a UK sort code and account number. This means your IBAN begins with GB, the same as any other UK bank account. Payroll, direct debits and standing orders all work exactly as they would with a high-street current account. There is no waiting period for the sort code and account number: they are issued on the same screen that confirms your account is active. The physical debit card arrives by post within a few working days.

There is no minimum opening deposit. There is no notice period for closing the account. Kroo is designed to be picked up and put down with minimal friction, and the opening process reflects that philosophy throughout.

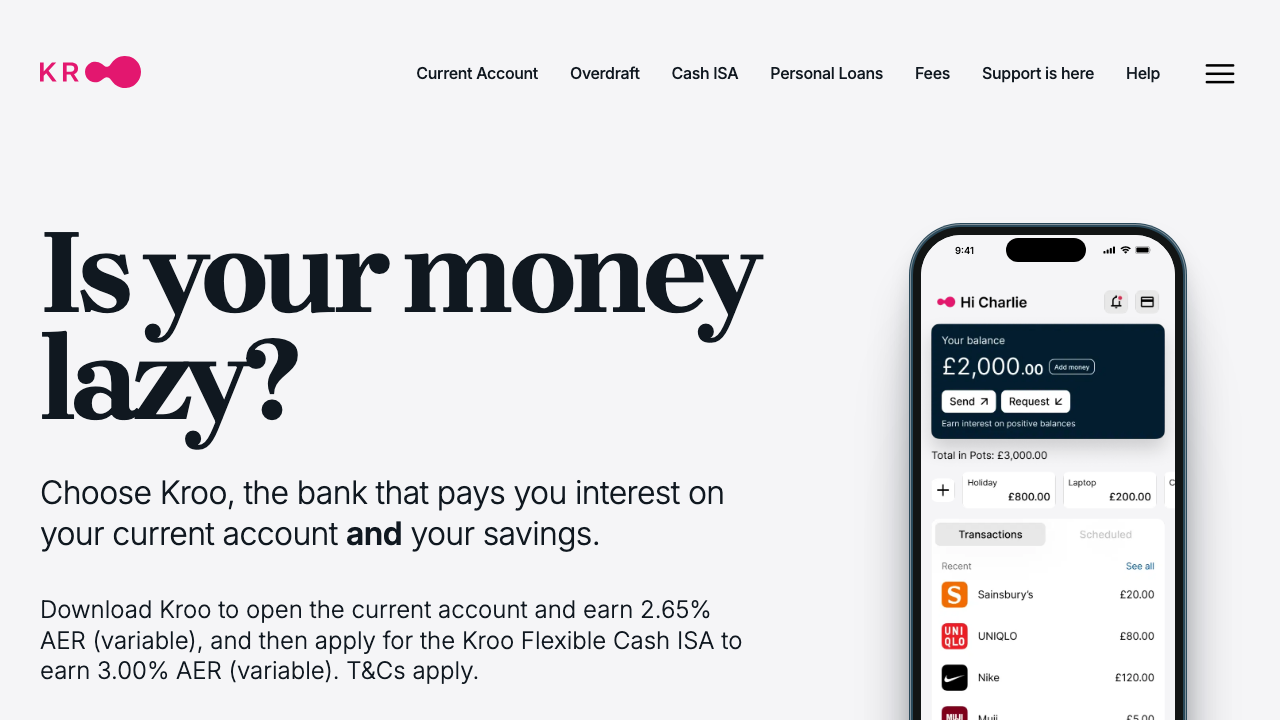

The app, interest on balances and customer service

Kroo’s app is clean and fast. The interface prioritises clarity over feature density, which is consistent with what a relatively young bank can actually build and maintain at a high standard. Spending categorisation happens automatically, and the transaction feed is grouped by merchant rather than presented as a raw list of debits. For anyone who budgets seriously, the categories are a useful starting point, though they lack the granular tagging options found in some more mature apps.

One feature that genuinely distinguishes Kroo from most current account providers is the credit interest paid on balances held in the account. Most current accounts pay nothing on balances above zero; Kroo pays interest on the full positive balance. The rate is variable and subject to change, so it is worth checking the current figure directly with Kroo before opening. The interest is paid monthly and appears as a credit on the account statement. For someone maintaining, say, a £3,000 float in their everyday account, this is money that would otherwise sit idle.

Customer service runs entirely through in-app messaging. There is no telephone support. For straightforward queries, the response times during working hours are reasonable, and the tone is notably less scripted than most large bank contact centres. The weakness is availability during evenings and weekends, where response times stretch. If you need to dispute a payment or resolve an urgent card issue outside business hours, you can freeze the card immediately in the app, but you may wait longer for a human response than you would with a bank that has 24-hour telephone support.

Reputation and real customer experience

Kroo’s public review profile is broadly positive, with recurring praise focused on a specific set of themes. Account opening speed and the absence of unexpected fees come up repeatedly. Travellers consistently mention the foreign spending terms as a practical benefit they notice in real use. The app design draws positive comments for its simplicity, particularly from users moving from traditional banks.

The recurring criticisms are also consistent and worth taking seriously. The most common complaint concerns customer service response times outside core hours. A smaller number of users report frustration with the lack of an overdraft facility, which means the account is unsuitable as a sole account for anyone whose cash flow is unpredictable month to month. There are also occasional mentions of the limited product range: no savings account with a fixed rate, no credit card, no joint account offering that matches what the largest challengers provide.

It is worth noting that Kroo is a young bank still building out its product set. Some of the gaps customers report today may not exist in twelve months’ time. The bank is candid about its roadmap in its public communications, which is a reasonable sign of institutional transparency. What you should not do is open a Kroo account expecting a feature set that rivals Starling or Monzo’s current breadth, because it is not there yet.

Verdict: open a Kroo account or look elsewhere?

Kroo earns a place in the shortlist of UK challenger current accounts for two reasons that are harder to find together than they appear: a zero-fee structure with no foreign transaction charges, and credit interest paid on the balance you hold in your everyday account. Neither feature is unique on its own, but the combination in a single, FCA-regulated, FSCS-backed account is genuinely useful.

Open a Kroo account if you travel several times a year and want a card that works abroad without penalty, if you keep a meaningful balance in your current account and want some return on it, or if you are simply done with paying monthly fees for a basic banking service that should be free.

Look elsewhere if you need a branch, require an overdraft, want a savings account and a current account from one provider, or need 24-hour telephone support. Monzo and Starling both offer a broader product suite for customers whose needs extend beyond the core current account. For those who want to earn the highest possible rate on a UK balance rather than have it sit in a current account, a dedicated easy-access savings account from a specialist provider will outperform anything a current account can offer. Kroo is not trying to be everything. For what it does do, it does it well.

How safe is Kroo Current Account?

Kroo Current Account vs alternatives

A direct comparison of the key conditions against the strongest competitors in the market.

Kroo Current AccountReviewed Kroo Current AccountReviewed | Monzo Current Account | Starling Current Account | Chase Current Account | |

| Rating | 4.0 /5 | 5.0 /5 | 5.0 /5 | 5.0 /5 |

| Monthly fee | £0/month | £0/month | £0/month | £0/month |

| Debit card | ✓ | ✓ | ✓ | ✓ |

| Credit card | ✗ | ✗ | ✗ | ✗ |

| Apple Pay | ✓ | ✓ | ✓ | ✓ |

| Google Pay | ✓ | ✓ | ✓ | ✓ |

| Cash withdrawal abroad | Free (no Kroo fees) | Free up to £400/30 days; then 3% (outside EEA) | Free (no Starling fees) | Free up to £500/month; then 1.5% |

| Online account opening | ✓ | ✓ | ✓ | ✓ |

| Deposit protection | 85.000 | 85.000 | 85.000 | 85.000 |

| iOS app | ✓ | ✓ | ✓ | ✓ |

| Branches | ✗ | ✗ | ✗ | ✗ |

How we rate

About the author

Frequently asked questions

You must be a UK resident and at least 18 years old to apply. The application is completed entirely through the Kroo app using a valid UK passport or driving licence for identity verification. Applicants outside the UK are not currently eligible.

No. The Kroo Current Account carries a £0 monthly fee with no conditions attached, no minimum deposit, and no salary requirement. Overseas card spending and ATM withdrawals abroad are also free of Kroo's own charges.

Yes. Kroo holds a full UK banking licence and deposits are covered by the FSCS (Financial Services Compensation Scheme) up to 120,000 GBP per person per bank. This is the standard UK deposit protection limit, the same level as any high-street bank.

Download the Kroo app on iOS or Android, enter your details, and verify your identity with a photo of your UK passport or driving licence plus a selfie video. Most applications are approved within minutes and your UK account number and sort code are available immediately.

Kroo is authorised and regulated by the FCA and PRA, the UK's main financial regulators. It is a fully licensed bank, not an e-money institution, which means your balance benefits directly from FSCS deposit protection rather than being held in a client-funds pool.

Interest paid on the Kroo current account balance counts as savings income for UK tax purposes and falls under the Personal Savings Allowance. Basic-rate taxpayers can receive up to £1,000 in interest per tax year free of income tax; higher-rate taxpayers have a £500 allowance. Interest above those thresholds is subject to income tax at your marginal rate.