Zuletzt aktualisiert:

A current account is the bank account most people in the UK use for everyday money. It’s the account your salary lands in, the account your rent and bills come out of, and the account tied to the debit card in your wallet. Unlike a savings account, it isn’t built to grow your money. It’s built to move money in and out with as little friction as possible.

Banks sometimes call this a “personal account” or, in the United States, a “checking account.” Whatever the label, the job’s the same: hold your everyday cash and let you spend it, transfer it, or pay bills with it on demand.

What is a current account?

A current account is a bank account designed for regular, everyday transactions rather than long-term saving. You use it to receive your salary or benefits, pay bills, withdraw cash, and spend using a linked debit card. Most UK adults hold at least one, and if you’ve ever been paid a wage, that’s almost certainly where it landed.

The word “current” refers to the money moving through the account in its everyday use, not sitting untouched the way savings might. That’s also why current accounts typically pay little or no interest. The bank expects the balance to move, not to build up.

What features come with a current account?

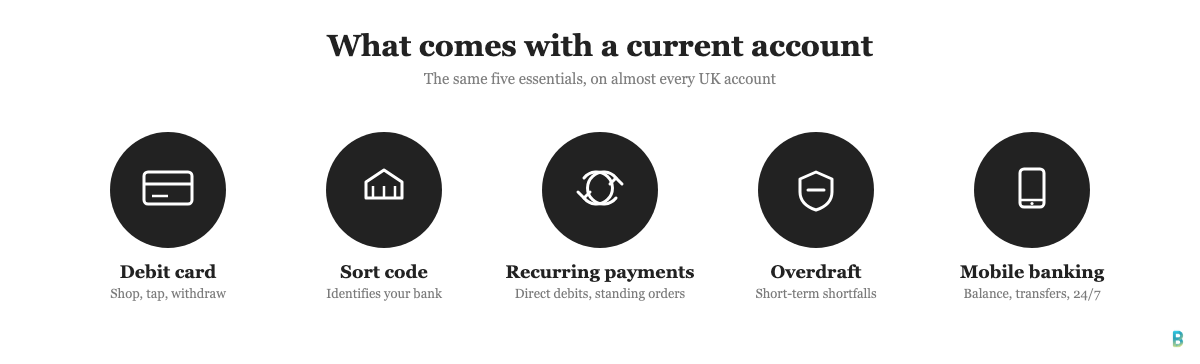

Nearly every current account in the UK comes with the same core toolkit, even though the branding differs from bank to bank. It doesn’t matter which provider you pick. Here’s what you’ll almost always get:

- A debit card for in-store and online purchases, plus cash withdrawals at ATMs

- A unique account number and sort code so people can pay money into your account

- Direct debits and standing orders for recurring payments

- An overdraft facility, arranged or unarranged, for short-term shortfalls

- Online and mobile banking so you can check your balance and move money at any time

Standing orders vs direct debits: what’s the difference?

A standing order is a payment you set up and control yourself. You tell your bank to send a fixed amount to someone else on a schedule you choose, which makes it useful for rent or a regular saving transfer. A direct debit works the other way round: you authorise a company, such as an energy supplier or a gym, to collect a payment from your account, and the amount can vary each time. The difference comes down to who’s in charge of the payment. You control a standing order. The company controls a direct debit.

Do current accounts cost anything?

Most current accounts are genuinely free to run as long as you stay in credit, so there’s often nothing to pay at all. Costs tend to appear at specific moments rather than as a flat monthly charge:

- Interest on an arranged overdraft, and a steeper fee if you slip into an unarranged one

- Charges for spending abroad on a standard debit card, depending on the provider

- Fees for sending large sums or making international transfers

- A monthly fee on packaged accounts, typically £2 to £20, in exchange for perks such as travel insurance or breakdown cover

If you never use an overdraft, rarely spend abroad, and stick to a fee-free account, day-to-day banking can genuinely cost nothing at all.

What types of current account are available?

Current accounts come in several common shapes, and most UK banks don’t just offer one.

| Account type | Who it suits | Typical features |

|---|---|---|

| Standard current account | Most everyday customers | Debit card, arranged overdraft option, no monthly fee |

| Basic bank account | People who can’t get a standard account, often due to credit history | Debit card, no overdraft, sometimes no chequebook |

| Packaged account | Customers who want bundled perks | Monthly fee, travel insurance, breakdown cover, retail discounts |

| Joint account | Couples, housemates, or family members sharing costs | Two or more named holders, shared access to funds and statements |

| Student account | Students in higher education | Interest-free overdraft limit, sign-up perks such as railcards |

A smaller number of providers, mostly app-based banks, also offer accounts built for specific groups. Think a youth account for younger teenagers with parental controls, or a lightweight account for freelancers and sole traders who want to separate business income from personal spending. If you’re heading to university, it’s worth checking a dedicated student bank account first, since these typically add an interest-free overdraft and sign-up perks that a standard account won’t.

If you’re ready to compare specific providers rather than just account types, bankinggeek.com’s guide to the best current accounts in the UK ranks the leading options by fees, app quality, and switching bonuses.

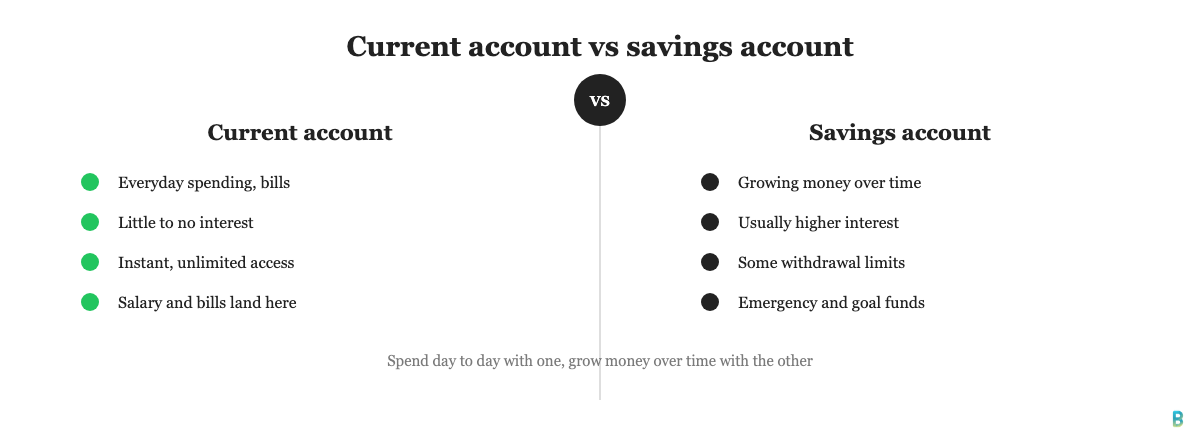

What’s the difference between a current account and a savings account?

A current account is built for spending. A savings account is built for storing money and earning interest. You can withdraw from a current account as often as you like, usually with no notice, while some savings accounts limit withdrawals or ask for advance notice in exchange for a better rate.

| Current account | Savings account | |

|---|---|---|

| Main purpose | Everyday spending and bill payments | Growing money over time |

| Interest | Little to none on most accounts | Usually higher, sometimes tiered |

| Access | Instant, unlimited in most cases | Often instant, but some accounts restrict withdrawals |

| Typical use | Salary, bills, day-to-day spending | Emergency fund, short or long-term goals |

If you’re holding money you won’t touch for a while, a savings account will almost always earn more, period. If you need to move money freely day to day, a current account is clearly the right tool, and there isn’t really a substitute for it.

Who can open a current account and what do you need?

Most UK banks let you open a current account from age 16, though some set the bar at 18, and a parent or guardian is often involved for younger applicants. Beyond age, providers usually ask for:

- Proof of identity, such as a passport or driving licence

- Proof of address, such as a recent utility bill or bank statement

- Basic personal details, including your name, date of birth, and contact information

Most applications happen online or through an app and don’t take more than a few minutes to submit. Approval for a new customer can take up to ten working days, though it’s often much faster, and existing customers switching products can sometimes be approved within a day. A standard credit check usually forms part of the process, even though a current account isn’t a loan.

Is my money safe in a current account?

Yes, money held in a current account with an authorised UK bank or building society is protected by the Financial Services Compensation Scheme (FSCS). Since 1 December 2025, the scheme has protected eligible deposits up to £120,000 per person, per authorised institution, so your everyday balance stays covered even if the bank fails. That protection is entirely automatic and non-negotiable. You don’t need to apply for it or ask your bank to switch it on, and no provider can opt out of it.

Joint accounts are treated slightly differently: each named holder typically gets their own £120,000 of protection on the same account, effectively doubling the cover. It’s worth checking that your bank and any other accounts you hold aren’t secretly sharing one licence, since some banking brands share the same authorisation and therefore share a single protection limit.

Frequently asked questions about current accounts

Is a current account the same as a checking account?

Yes, a current account is simply the UK term for what American banks call a checking account, and the two are functionally identical. Both describe the same kind of everyday account used for spending, direct debits, and salary payments rather than saving.

Do current accounts pay interest?

Most current accounts pay little or no interest, since they’re designed for spending rather than saving. A handful offer a small rate on balances up to a set limit, but if earning interest’s your priority, a savings account will usually pay more.

Can I have more than one current account?

Yes, there’s no legal limit on how many current accounts you can hold, full stop. Plenty of people keep two or three for different purposes, such as separating bills from spending money, though banks may still run their own eligibility checks each time you apply.

How long does it take to switch current accounts?

Switching under the Current Account Switch Service usually takes seven working days from start to finish. Your new bank handles the move, so you don’t have to chase old direct debits, standing orders, or incoming payments yourself, and nothing gets missed. Our full guide to switching bank accounts walks through each step, plus which providers currently pay a cash bonus for moving your account.

What is the minimum age to open a current account?

Most banks set the minimum age at 16 or 18, depending on the provider and the type of account. Some banks offer accounts for younger teenagers with parental controls, while standard adult current accounts are usually reserved for those 18 and over.

What is a sort code?

A sort code is a six-digit number, usually written as three pairs, that identifies your bank and the specific branch or division your account is held with. You’ll need it alongside your account number any time someone pays money into your account by bank transfer.

Can I get a current account with a poor credit history?

Yes, most UK banks offer a basic bank account specifically for people who can’t pass the credit check needed for a standard account. It won’t come with an overdraft or a chequebook, but it still gives you a debit card, a sort code, and the ability to receive payments and pay bills.