Tandem Bank Tandem Savings Account: review 2026

Last updated: 13.06.2026

Contents

Summary

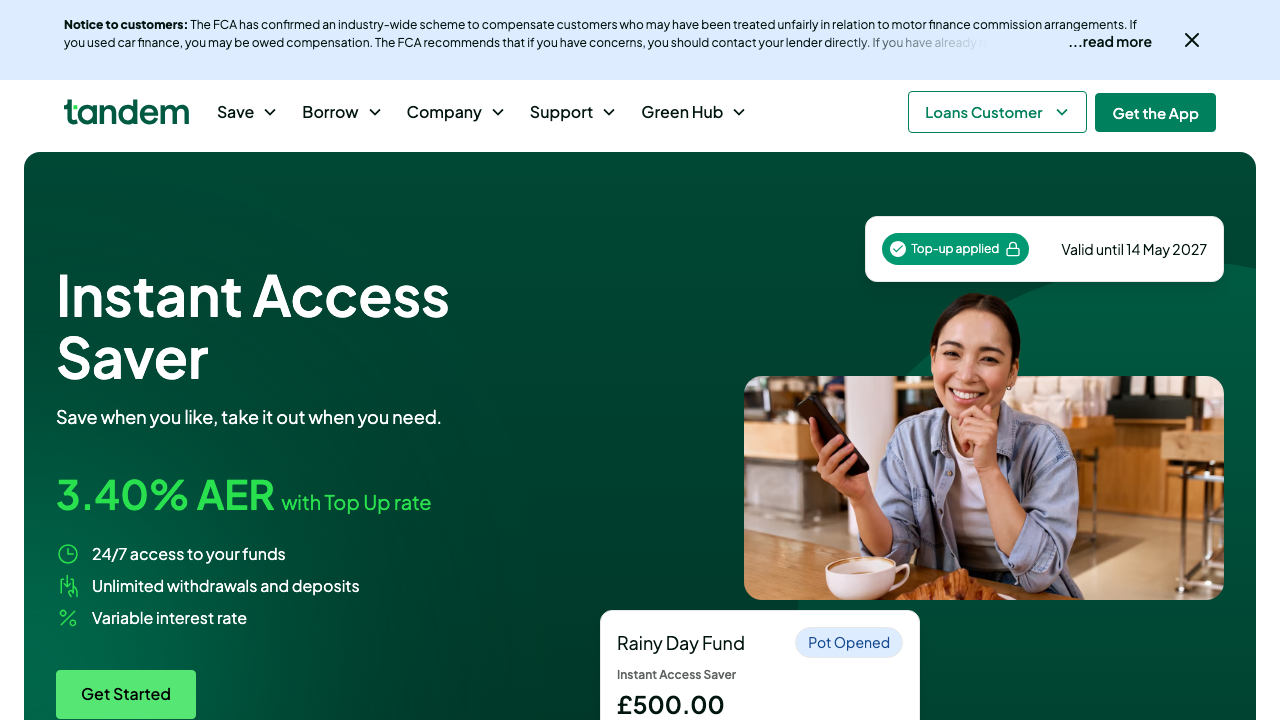

The Tandem Bank Savings Account is a fully digital instant-access saver paying 3.40% AER variable, which includes a 12-month Top Up bonus for new customers. It suits savers who want a quick, paperless setup and are comfortable managing everything through a smartphone app. The absence of a current account or joint account option means it works best as a standalone savings pot rather than a primary banking relationship.

Pros

- Competitive instant-access rate of 3.40% AER variable including a 12-month Top Up bonus

- no minimum deposit required and balances up to £250,000 accepted

- account opened in minutes via app using Open Banking identity verification

- FSCS protection up to £120,000

- green banking model with savings channelled into sustainable lending projects

Cons

- No joint savings accounts available

- deposits restricted to a linked UK bank account only

- standard variable rate falls once the 12-month Top Up period expires

- no current account or debit card offered alongside the saver

Key facts

| Interest on savings account | 3.40% AER variable (incl. 12-month Top Up) |

| Deposit protection | 120.000 GBP |

| Online account opening | ✓ |

| Welcome bonus | ✗ |

| Joint account | ✗ |

| Overdraft interest rate | ✗ |

| Savings account | ✓ |

| Rating | 3.9 /5 |

Interest rate comparison

The effective annual rate compared directly with the alternatives.

A closer look

Overview: what the Tandem Savings Account offers and who it suits

Tandem Bank positions itself as one of the UK’s few dedicated green challenger banks, and its Instant Access Saver sits at the heart of what it does. The account pays 3.40% AER variable, a rate that includes a 12-month Top Up bonus layered on top of the underlying variable base. There is no minimum opening deposit, balances up to £250,000 are accepted, and the whole process runs through a smartphone app with Open Banking identity checks. It is fully covered by the Financial Services Compensation Scheme up to £85,000 per depositor.

The account works well for savers who want a straightforward, app-first home for their cash, care about where their money goes, and are comfortable with a purely digital experience. The green angle is genuine rather than marketing gloss: Tandem publicly directs savings deposits into home improvement loans and other sustainability-linked lending. In our test, opening the account took under ten minutes from download to funded balance, which is among the fastest we have encountered for a UK savings product.

It is not for everyone, though. If you need a joint account, you will need to look elsewhere. Deposits can only be sent from a linked UK bank account, so anyone relying on transfers from overseas accounts or non-standard payment sources will hit a wall. There is no current account, no debit card, and no branch network. Savers who prefer face-to-face service or want to manage everything through one banking app will find Tandem limited by design.

The interest rate in detail: Top Up bonus, base rate and what happens after 12 months

The headline 3.40% AER variable is a blended figure. Tandem operates a two-layer structure: a base variable rate and a 12-month Top Up bonus that sits on top for new customers. The combined figure at launch is 3.40% AER. Once the bonus period expires, the rate reverts to the underlying variable rate, which Tandem can change at any time in line with market conditions.

Interest is calculated daily and credited to the account monthly. There are no fees tied to the rate, no minimum monthly funding requirement, and no penalty for withdrawals. This is a true instant access product, meaning you can move money out at any point without losing accrued interest for the period you held funds. The AER and gross rate are the same because interest is paid once a year on an equivalent basis, though Tandem credits monthly in practice.

The variable structure matters. Rates on instant access accounts across the UK market have been shifting sharply since the Bank of England began its cutting cycle, and Tandem’s base rate will move with it. Savers who want certainty over a defined term should consider a fixed-rate bond instead. For those who prioritise flexibility over rate lock-in, the instant access structure is the right fit, but they should revisit the rate once the Top Up bonus drops off and benchmark against current market offers at that point.

UK taxation of savings interest: Personal Savings Allowance and what Tandem pays

In the UK, savings interest is taxed through the income tax system, not at source. Basic-rate taxpayers (20%) receive a Personal Savings Allowance of £1,000 per year. Higher-rate taxpayers (40%) get £500. Additional-rate taxpayers (45%) receive no allowance at all. Tandem pays interest gross, without deduction, and it is the account holder’s responsibility to declare any interest above their allowance through self-assessment or by contacting HMRC if they are PAYE-only.

At 3.40% AER on a £29,412 balance, a basic-rate taxpayer would hit the £1,000 allowance precisely. Most savers holding less than that will pay no tax on Tandem interest at all. Higher earners or those holding larger balances should factor in the tax drag when comparing net returns across providers. Cash ISAs, by contrast, shelter interest entirely from income tax, which is why alternatives such as Trading 212 Cash ISA or Moneybox Cash ISA appear in the comparison landscape for this account.

Tandem does not issue a tax certificate automatically at year end; savers will need to retrieve interest statements from the app. HMRC receives bank interest data directly from providers in many cases, but self-employed savers and those with complex income should not rely on that and should keep their own records.

Opening the account: step by step, identification and funding

The application is entirely app-based. Download the Tandem app from the App Store or Google Play, select the Instant Access Saver, and begin the identity check. Tandem uses Open Banking-linked verification rather than document upload or video call, which means the process connects briefly to your existing UK bank account to confirm identity. This is fast but does require that your current bank supports Open Banking, which covers all major UK providers.

Once identity is confirmed, you link a UK bank account for deposits and withdrawals. This linked account is the only source from which funds can enter or leave the Tandem account. You can change the linked account later, but only one account can be active at a time. In our test, the full journey from app download to an active, funded account ran to around eight minutes.

There is no lock-in period and no notice requirement. Withdrawals are processed to the linked account, typically arriving the same working day. There is no minimum deposit to open, and no requirement to fund immediately after account creation. Balances up to £250,000 are accepted, though only the first £85,000 falls within FSCS protection.

Safety: FSCS protection and the bank behind the account

Tandem Bank is authorised and regulated by the Financial Conduct Authority and the Prudential Regulation Authority, and it holds a full UK banking licence. That licence matters: it means deposits are protected by the Financial Services Compensation Scheme up to £85,000 per eligible depositor. If Tandem were to fail, HMRC would not be involved in the compensation process; the FSCS pays out directly, typically within seven working days under current rules.

The £85,000 FSCS limit applies across all accounts you hold with Tandem Bank, not per account. Savers with more than £85,000 to deposit should be aware that only the first £85,000 is protected; the remaining balance in a single-bank failure scenario would be an unsecured creditor claim. Spreading balances across multiple FSCS-authorised providers is the standard approach for larger sums.

Tandem itself was founded in 2013, received its full banking licence in 2017, and rebranded with a green focus following the acquisition of Harrods Bank’s savings book in 2018. It is a relatively small institution by UK banking standards, which is neither a red flag nor a guarantee, but savers should note it does not carry the balance sheet depth of a high-street bank. The regulatory framework, not balance sheet size, is the relevant safety layer here.

Reputation and real customer experience: what users praise and where friction appears

Across public review platforms, Tandem’s savings account draws consistent praise for two things: the speed and simplicity of opening, and the lack of friction around withdrawals. Customers frequently note that pulling money out is as quick as putting it in, which is the core promise of an instant access product and one Tandem appears to deliver reliably.

The green angle also features positively in reviews, particularly among savers who want their money to fund something tangible rather than sitting in a generic pool. Tandem’s messaging around home improvement and energy efficiency lending resonates with this segment, and there is no sense from customer accounts that the sustainability narrative is purely cosmetic.

Recurring criticisms follow a narrower pattern. The restriction to a single linked UK account draws complaints from savers who want more flexibility over funding sources, particularly those who maintain accounts at multiple banks or who receive income in more than one place. Customer service response times are flagged as inconsistent: in-app chat works well for simple queries but escalations to more complex issues can stretch. The absence of a joint account option is a firm and unresolved gap for couples managing savings together. A handful of users also report surprise when the Top Up bonus expires and the rate drops without a prominent in-app notification, which is a product design point rather than a regulatory issue but worth noting.

Verdict: who should open the Tandem Savings Account and who should look elsewhere

Tandem’s Instant Access Saver is a solid option for individual UK savers who want a competitive variable rate, no minimum deposit, instant access and a clean app experience, and who are comfortable with the green banking proposition. The 3.40% AER is competitive within the instant access segment for 2026, and the Open Banking onboarding is among the smoothest available for a regulated savings account.

The account earns its place in a savings portfolio as a flexible, accessible holding account rather than a primary long-term savings vehicle. Its variable rate structure and the expiry of the Top Up bonus after 12 months mean it rewards active management: set a calendar reminder for when your bonus period ends and compare rates again at that point.

Look elsewhere if you need a joint account, if your income arrives from non-UK accounts, if you want to shelter interest inside an ISA wrapper, or if you prefer a bank with a current account attached. The Skipton Building Society and other mutual providers offer competitive notice accounts and fixed-term bonds for savers who want rate certainty. Cash ISA providers such as Trading 212 or Moneybox are more relevant if tax efficiency is the priority. Tandem does one thing well: simple, app-only instant access savings with a green purpose. If that matches your situation, it is worth considering.

How safe is Tandem Bank Tandem Savings Account?

Tandem Bank Tandem Savings Account vs alternatives

A direct comparison of the key conditions against the strongest competitors in the market.

Tandem Bank Tandem Savings AccountReviewed Tandem Bank Tandem Savings AccountReviewed | Trading 212 Cash ISA | Moneybox Cash ISA | Skipton Building Society Savings Account | |

| Rating | 3.9 /5 | 4.5 /5 | 4.3 /5 | 4.2 /5 |

| Interest on savings account | 3.40% AER variable (incl. 12-month Top Up) | 4.81% AER variable (incl. 0.71% bonus for 12 months; standard rate 4.10% AER) | 4.75% AER variable (incl. 1.30% bonus for 12 months) | ca. 3.85% AER variable (Easy Access Saver); up to 7.50% AER (Member Regular Saver, 12 months) |

| Deposit protection | 120.000 GBP | 120.000 GBP | 120.000 GBP | 120.000 GBP |

| Online account opening | ✓ | ✓ | ✓ | ✓ |

| Welcome bonus | ✗ | ✓ | ✗ | ✗ |

| Joint account | ✗ | ✗ | ✗ | ✓ |

| Overdraft interest rate | ✗ | ✗ | ✗ | ✗ |

| Savings account | ✓ | ✓ | ✓ | ✓ |

How we rate

More comparisons

About the author

Frequently asked questions

The account is open to UK residents aged 18 or over who hold an existing UK bank account. Applicants must download the Tandem app and complete identity verification through Open Banking using their existing account.

No. There are no monthly fees, no withdrawal charges, and no minimum balance requirement. The account is free to hold, and the only cost is the opportunity cost if the variable rate falls after the 12-month Top Up bonus period ends.

Deposits are covered by the FSCS (Financial Services Compensation Scheme) up to £120,000 per person per bank. Tandem Bank is authorised by the PRA and regulated by the FCA. Balances above the £120,000 limit are not protected by the scheme.

Download the Tandem app, enter your details, and verify your identity by linking an existing UK current account through Open Banking. The entire process takes around five minutes and does not require any document uploads or branch visits.

Tandem Bank is a fully authorised UK bank regulated by the FCA and PRA. Deposits up to £120,000 are FSCS-protected. The bank has operated since 2014 and focuses on green lending, primarily sustainable mortgages.

Interest is paid gross and falls under the UK Personal Savings Allowance: £1,000 per year for basic-rate taxpayers and £500 for higher-rate taxpayers. Tandem reports interest paid to HMRC, and tax is usually collected via your PAYE tax code rather than through self-assessment.