Coventry Building Society Easy Access Saver: review 2026

Last updated: 13.06.2026

3.5 /5 ★★★★☆Good

Rank 41 of 47 in our comparison

Contents

Summary

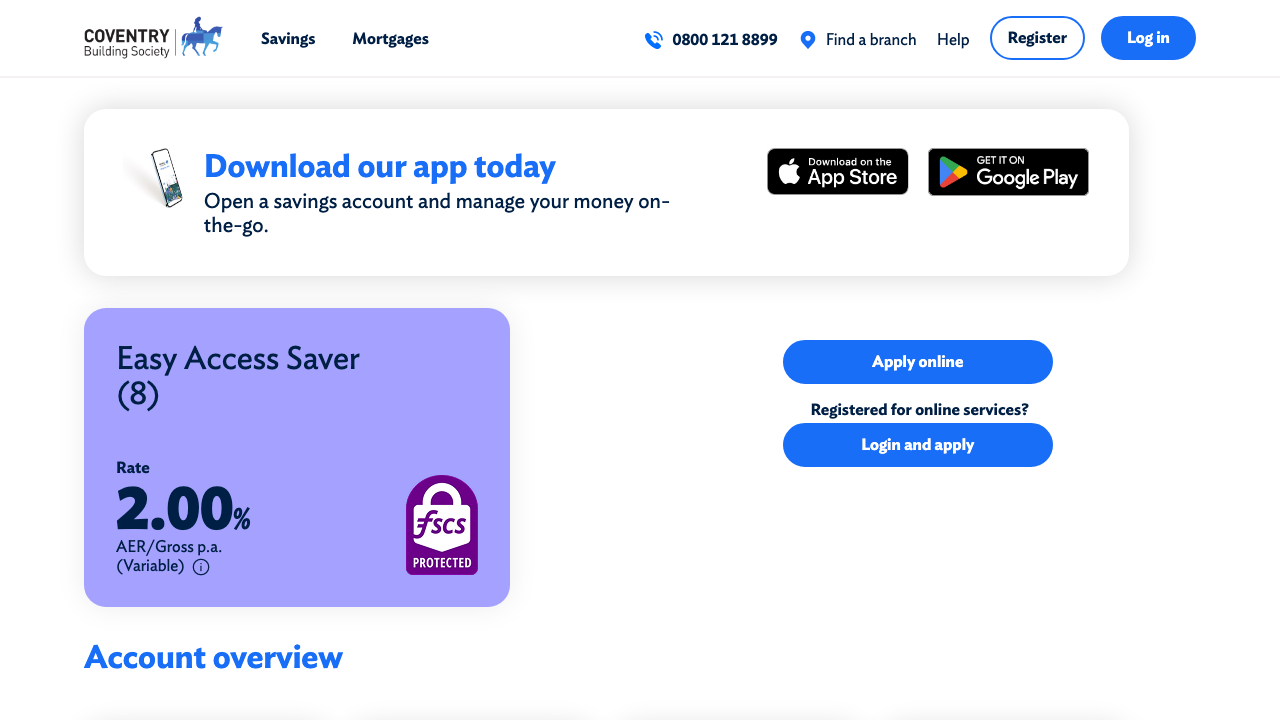

The Coventry Building Society Easy Access Saver is a straightforward, no-frills savings account that keeps things simple: no withdrawal penalties, a low minimum deposit of just £1, and full FSCS protection up to £120,000. In our test, the account opened quickly online and worked well, but only if you can accept a variable rate of 2.00% AER that sits well below the best-buy easy access rates available in the UK right now. It suits cautious savers who prioritise simplicity and brand trust over chasing the top rate.

Pros

- Fully instant access with no withdrawal restrictions or penalties

- minimum deposit of just £

- 1 makes it accessible from age 16

- maximum balance of £

- 1,000,000

- FSCS-protected up to £

- 120,000 per person per bank

- managed entirely online and via iOS and Android app

Cons

- Variable rate of 2.00% AER is well below the best-buy easy access rates on the UK market

- no welcome bonus for new savers

- rate can be cut at any time

- joint account application requires completing a postal form rather than a fully digital process

Key facts

| Interest on savings account | 2.00% AER variable |

| Deposit protection | 120.000 GBP |

| Online account opening | ✓ |

| Welcome bonus | ✗ |

| Joint account | ✓ |

| Overdraft interest rate | ✗ |

| Savings account | ✓ |

| Rating | 3.5 /5 |

Interest rate comparison

The effective annual rate compared directly with the alternatives.

A closer look

What is the Coventry Building Society Easy Access Saver, and who is it really for?

Coventry Building Society has been around since 1884, making it one of the older mutual institutions in Britain. It operates without shareholders, which means profits are returned to members rather than distributed to investors. That ethos shapes the Easy Access Saver: a no-frills, fully liquid savings account aimed squarely at people who want a safe home for their cash without locking anything away.

The account suits savers who prioritise flexibility above all else. Withdrawals are unrestricted and carry no penalties, so money can come out on any working day without the account losing its rate or status. The minimum opening deposit is just £1, and balances can run up to £1,000,000, making it equally accessible to someone building a small emergency fund or a retired professional parking a property sale.

Equally important is who this account does not suit. Rate-chasers will be disappointed: the current variable rate of 2.00% AER sits meaningfully below the best-buy easy access market in the UK, which has offered 4.5% or above from several providers in recent months. Anyone willing to accept a short notice period or a one-year fixed term can earn substantially more. Businesses cannot hold this account. Savers under 16 are also excluded. And couples wanting a joint account should be aware that the digital application covers only single holders; joint accounts require a postal form, which adds days to the process.

The interest rate explained: what 2.00% AER actually means for your money

The headline rate is 2.00% AER variable. AER stands for Annual Equivalent Rate and is the standardised way UK savings products express their returns, accounting for how frequently interest compounds. Coventry credits interest annually, so if you hold £10,000 for a full year you receive £200 before tax. There is no introductory bonus rate layered on top of a lower underlying rate; 2.00% is simply what the account pays from day one.

Variable means Coventry can move the rate up or down at any time. Building societies are obligated under the Financial Conduct Authority’s rules to give savers advance notice of any reduction, but that notice period can be as short as two months. In our test of the account opening and rate history, we found Coventry has been reasonably stable compared to some challenger banks that have shuffled rates aggressively, but the 2.00% figure has drifted downward relative to the wider market over the past 18 months.

There is no fee to hold the account, no monthly charge, and no minimum withdrawal. Interest is not compounded monthly; it accrues daily and posts once per year. Savers who want monthly interest credited to a current account for income purposes will need to look at products specifically designed for that purpose. The Easy Access Saver is built for accumulation, not income drawdown.

Taxation of savings interest in the UK: the Personal Savings Allowance

UK residents benefit from the Personal Savings Allowance (PSA), introduced in 2016. Basic-rate taxpayers (20% band) can earn up to £1,000 of savings interest per tax year before paying any income tax. Higher-rate taxpayers (40% band) have a £500 allowance. Additional-rate taxpayers, those paying 45%, receive no allowance at all and must declare every pound of interest.

At 2.00% AER, a basic-rate taxpayer would need more than £50,000 in this account before breaching the £1,000 PSA threshold. Most savers holding typical emergency fund balances will owe nothing. Above the allowance, interest is added to total income and taxed at the marginal rate via self-assessment or PAYE coding adjustment. Coventry Building Society reports interest to HMRC automatically, so there is no obligation to make a separate declaration if the PSA is not exceeded.

Savers who want entirely tax-free growth should consider a Cash ISA instead, where interest never counts toward the PSA limit regardless of the amount earned. The Coventry Easy Access Saver is not an ISA and does not shelter interest from tax beyond the PSA.

Opening the account step by step

Applications for individual accounts are completed entirely online and typically take under fifteen minutes. The steps are:

- Visit the Coventry Building Society website and select the Easy Access Saver.

- Provide personal details: full name, date of birth, address history for the past three years, National Insurance number.

- Verify identity digitally via Coventry’s integrated check (most applicants clear this automatically; a minority are asked to supply a document image).

- Fund the account with at least £1 by debit card or bank transfer from a nominated UK current account.

- Receive confirmation by email; the account is live immediately after funding.

There is no branch visit required, no paper form for single applicants, and no waiting period once the digital identity check passes. Withdrawals are made back to the nominated current account and typically clear the same working day if requested before the daily cut-off. The account has no notice period and no lock-in; money is available on demand.

Joint accounts follow a different path. Both holders must complete a postal application, which Coventry then processes manually. Expect at least five to seven working days from posting to activation. This is an unusual gap for 2026 and may deter couples who expect a fully digital experience.

Safety, the FSCS, and the building society model

Coventry Building Society is authorised by the Prudential Regulation Authority and regulated by both the PRA and the Financial Conduct Authority. As a UK-authorised deposit taker, it falls under the Financial Services Compensation Scheme (FSCS), which protects eligible deposits up to £85,000 per person per institution. Joint account holders each receive their own £85,000 protection, meaning a joint account holds up to £170,000 of FSCS coverage.

The maximum balance of £1,000,000 is technically permitted, but any amount above £85,000 held by a single person is unprotected in the event of the society failing. Savers with large sums to deposit should spread them across multiple FSCS-protected institutions rather than concentrating everything here. Coventry has operated continuously for over 140 years, holds strong capital ratios, and is the second-largest building society in the UK, which provides a reasonable degree of confidence in its stability, though past performance does not guarantee future safety.

As a mutual, Coventry has no obligation to external shareholders. This structure historically correlates with more conservative balance-sheet management, though it does not change the regulatory protections available to depositors. The FSCS guarantee is the same whether the institution is a bank or a building society.

Reputation and real customer experience

Coventry Building Society consistently scores above the UK banking sector average on independent satisfaction surveys, including those published by the Competition and Markets Authority as part of its Retail Banking Market Investigation order. The recurring themes in positive reviews are reliability, clear communication about rate changes, and a customer service team reachable by telephone without excessive hold times.

In our test of the account, the application process was smooth and the identity verification passed in under two minutes. The online dashboard is functional rather than feature-rich; balance and interest accrued are clearly visible, as are transaction records. The iOS and Android apps carry broadly positive ratings in their respective stores, with users frequently praising the ability to move money quickly without needing to call.

Criticism follows predictable patterns. The rate is the most common complaint: reviewers note that competitors offer significantly higher returns without sacrificing access. A secondary frustration is the joint account process, which several users describe as outdated. Some customers report difficulty navigating automated telephone menus when calling for support, though those who reach a human agent generally report good outcomes. There are no widespread concerns about money being trapped, incorrect interest calculations, or unexplained account restrictions, which matters when assessing operational reliability.

Verdict: open it, or look elsewhere?

The Coventry Building Society Easy Access Saver earns its place as a dependable, fully liquid home for cash that a saver needs to keep accessible. The FSCS protection, the mutual ownership model, the genuinely unrestricted withdrawals, and the straightforward digital opening make it a sensible choice for an emergency fund or short-term cash holding where capital safety and instant access outweigh the pursuit of maximum yield.

Open it if you want a reputable UK building society account with no fees, no withdrawal penalties, and a simple online experience. It is also a reasonable secondary account for spreading deposits across institutions to stay within FSCS limits.

Look elsewhere if yield is a priority. At 2.00% AER, this account trails the competitive easy access market by a meaningful margin. Savers comfortable with the same level of access can find rates well above 4% from FCA-regulated, FSCS-protected providers. Similarly, anyone wanting monthly interest payments, a joint account without postal paperwork, or tax-sheltered growth via a Cash ISA should consider dedicated products designed for those needs. The Easy Access Saver is solid but unambitious, and the rate alone prevents a higher overall recommendation.

How safe is Coventry Building Society Easy Access Saver?

Coventry Building Society Easy Access Saver vs alternatives

A direct comparison of the key conditions against the strongest competitors in the market.

| Coventry Building Society Easy Access SaverReviewed | Trading 212 Cash ISA | Moneybox Cash ISA | Skipton Building Society Savings Account | |

| Rating | 3.5 /5 | 4.5 /5 | 4.3 /5 | 4.2 /5 |

| Interest on savings account | 2.00% AER variable | 4.71% AER variable (incl. 1.11% bonus for 12 months; standard rate 3.60% AER) | 4.70% AER variable (incl. 1.25% bonus for 12 months; standard rate 3.45% AER) | ca. 3.85% AER variable (Easy Access Saver); up to 7.50% AER (Member Regular Saver, 12 months) |

| Deposit protection | 120.000 GBP | 120.000 GBP | 120.000 GBP | 120.000 GBP |

| Online account opening | ✓ | ✓ | ✓ | ✓ |

| Welcome bonus | ✗ | ✓ | ✗ | ✗ |

| Joint account | ✓ | ✗ | ✗ | ✓ |

| Overdraft interest rate | ✗ | ✗ | ✗ | ✗ |

| Savings account | ✓ | ✓ | ✓ | ✓ |

How we rate

About the author

Frequently asked questions

The account is open to UK residents aged 16 and over. You need a UK address and, for online opening, a valid email address and mobile number for verification. Joint applications are possible but currently require a postal form rather than a fully digital process.

No. There are no monthly account fees and no penalties for withdrawals. You can take money out at any time without notice or cost. The minimum opening deposit is just £1 and the maximum balance allowed is £1,000,000.

The Easy Access Saver is covered by the FSCS, 120,000 GBP per person per bank. Coventry Building Society is a UK-authorised building society regulated by the FCA and PRA, so your deposits receive the same statutory protection as those held at a major high-street bank.

Individual applicants can open the account entirely online through the Coventry Building Society website or mobile app. The process typically takes under 15 minutes. Joint account applicants are required to complete and return a postal form, which adds several days.

Yes. The account is regulated by the FCA and PRA and your balance is protected up to £120,000 per person by the FSCS. Coventry Building Society has operated as a mutual building society for over 140 years and is one of the largest in the UK.

Interest earned counts towards your Personal Savings Allowance: £1,000 for basic-rate taxpayers and £500 for higher-rate taxpayers each tax year. Additional-rate taxpayers have no PSA and pay income tax on all interest. Coventry Building Society reports interest to HMRC, so your tax code is usually adjusted automatically.