first direct 1st Account: review 2026

Last updated: 13.06.2026

Contents

Summary

The first direct 1st Account is a strong, phone-and-app-based current account from a division of HSBC, earning 4 out of 5 stars and 80 out of 100 points in our scoring. It suits people who want reliable, award-winning customer service without visiting a branch, provided they can meet the monthly funding requirement of at least £1,000. Linked extras such as a Regular Saver and a switching incentive make it particularly appealing as a primary account.

Pros

- Consistently top-rated customer service available 24/7 by phone

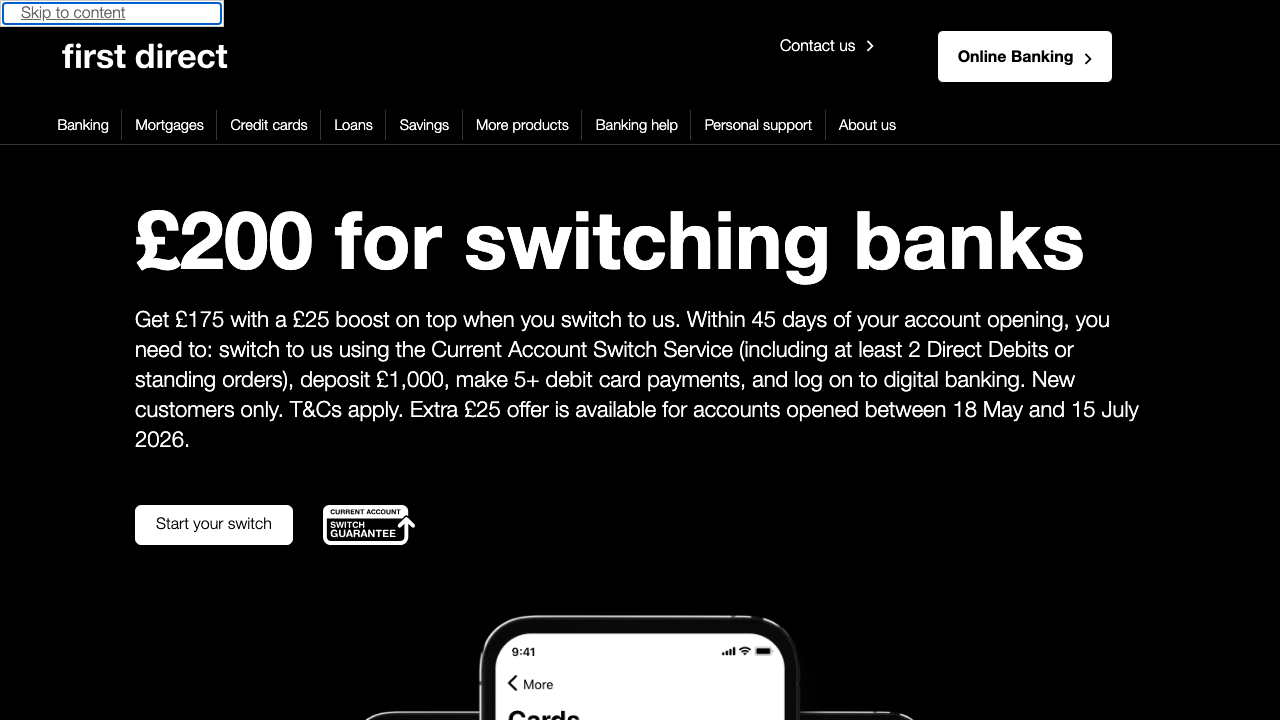

- Switching incentive available to eligible new customers

- Linked Regular Saver account with a competitive interest rate

- Apple Pay and Google Pay supported

- No first direct foreign currency fee on overseas spending

Cons

- £10 monthly fee applies if monthly deposits fall below £1,000

- No in-credit interest paid on the current account balance

- No physical branches (HSBC branches available for cash only)

- Switch incentive is subject to eligibility conditions

Key facts

| Monthly fee | £0/month (with monthly deposits >= £1,000; otherwise £10/month) |

| Debit card | ✓ |

| Credit card | ✗ |

| Apple Pay | ✓ |

| Google Pay | ✓ |

| Cash withdrawal abroad | Free (no first direct foreign currency fee; £1.50 ATM fee may apply) |

| Online account opening | ✓ |

| Deposit protection | 85.000 |

| iOS app | ✓ |

| Branches | Nein (Phone & App-Banking; HSBC-Filialen fuer cash) |

| Rating | 4.0 /5 |

Strengths in detail

How well the provider covers the most important areas.

A closer look

Overview: who the first direct 1st Account is for, and who it is not

first direct occupies an unusual corner of UK retail banking. Launched in 1989 as a subsidiary of HSBC, it stripped away branches entirely and built its proposition around telephone and, later, app-based service. That decision, radical at the time, turned out to be its lasting competitive edge: without branch overheads it has consistently channelled resources into staffing its contact centre with people who actually pick up the phone. The 1st Account is the flagship current account and the one most new customers open first.

The account suits salaried professionals and households that receive regular income. The monthly fee is £0 provided you pay in at least £1,000 each month. Miss that threshold and the fee becomes £10 per month, so anyone living on irregular freelance income or a low part-time wage faces a real cost. Students have dedicated products elsewhere on the high street; the 1st Account is not aimed at them. Equally, savers who want their everyday balance to earn interest will not find it here: the 1st Account pays no in-credit interest on the current account balance itself, so it functions as a transactional hub rather than a savings tool.

Where first direct shines is the ecosystem around the account. Opening a 1st Account unlocks access to the Regular Saver, which has historically carried one of the most competitive rates among high-street-linked savings products, and to a range of personal loans and mortgages on preferential terms. If you want one bank that does most things well and answers the phone at 3 am, first direct is worth serious attention.

Who should look elsewhere immediately: anyone who handles a lot of cash regularly (there are no first direct branches, though HSBC ATMs and branches accept deposits), people whose monthly income reliably falls below £1,000, and anyone whose entire banking relationship is online-only and brand-new to the UK with no existing credit history, since first direct does run a credit check on application.

Real costs and hidden fees in detail

The headline fee structure is straightforward. Pay in £1,000 or more each calendar month and the account costs nothing. Pay in less and the fee is £10 per month. That £1,000 threshold is based on total credits received, not on a single deposit, so multiple smaller payments from an employer, a side income, or a partner all count together. first direct has not historically been aggressive about adding ancillary charges, but there are a few worth knowing about.

Overseas ATM withdrawals carry a £1.50 fee per transaction. first direct does not add its own foreign-currency loading on top of the Mastercard exchange rate, which means the effective cost of spending abroad on the debit card is competitive compared with legacy banks. However, specialist travel cards from Starling or Chase will still typically be cheaper for heavy travellers because those providers absorb the ATM fee as well. Unarranged overdraft usage attracts a monthly charge rather than per-item fees; arranged overdraft interest is applied at a published annual rate. first direct has historically offered a small interest-free overdraft buffer to new customers, though the precise buffer amount has varied and should be confirmed at application.

Instant (Faster Payments) and CHAPS domestic transfers are handled through the normal online and app banking channels. Faster Payments are free and near-instant. CHAPS, used for high-value same-day transfers such as property completions, carries a fee that should be checked at the time of transfer. International SWIFT transfers are available but attract standard fees; for frequent international senders an account like Wise is more cost-efficient.

Cards and payments: debit card, mobile wallets, and limits

Every 1st Account comes with a Visa debit card. Credit cards are a separate product (the first direct Credit Card) and are not bundled with the current account. The debit card works on the Visa network worldwide, covering virtually all payment terminals and ATMs globally. Both Apple Pay and Google Pay are supported, so contactless payments via smartphone or smartwatch work without friction.

In our test, adding the card to Apple Pay took under two minutes: a push notification arrived, biometric confirmation was required, and the card was active in the Wallet immediately. Daily spending limits and ATM withdrawal limits are set by first direct and can generally be adjusted through the app or by calling the contact centre. Virtual card numbers for online purchases are not a feature of the 1st Account debit card at the time of writing; users concerned about online card security may want to consider a supplementary digital-only card from another provider for high-risk purchases, then keep the first direct card for primary day-to-day use.

Contactless limits follow the UK industry standard of £100 per transaction. PIN-verified payments have no fixed ceiling for point-of-sale use. For high-value purchases the bank may apply a real-time fraud check, occasionally triggering a text verification step. That is prudent security practice rather than a failing.

Opening the account step by step

Applications are completed entirely online at firstdirect.com or via the app. The process typically takes 10 to 15 minutes if you have the required documents to hand. You will need a UK address, a National Insurance number, and a form of photo ID. first direct accepts a UK passport or driving licence for identity verification; it does not operate in-branch ID checks because there are no branches. Verification is handled digitally, and in most cases an answer comes within minutes.

A credit and affordability check runs automatically at this stage. Applicants with a thin UK credit file (recent arrivals, for example) may be declined. Once approved, the sort code and account number are displayed in the app immediately; the physical debit card arrives by post within three to five working days. The IBAN for the account follows the UK format: GB followed by two check digits, then the six-digit sort code and eight-digit account number. This is fully compatible with international transfers and SEPA-adjacent payment systems that accept UK IBANs.

first direct is a participant in the Current Account Switch Service (CASS). Switching from another UK bank using CASS takes seven working days and automatically redirects all direct debits and standing orders. first direct periodically offers a cash incentive for new customers who switch via CASS; the incentive amount and conditions (minimum funding, debit card use within a set period) change from time to time, so check the current offer at point of application rather than relying on any figure quoted here. The account number and sort code assigned at opening are yours permanently.

App, features, and customer service quality

The first direct app is available on iOS and Android. It covers the essentials reliably: real-time balance and transaction history, Faster Payments, standing orders, direct debit management, and access to linked savings products. The interface is clean and functional rather than feature-saturated. You will not find budgeting breakdowns, round-up savings, or spending analytics of the kind offered by Monzo or Starling; first direct has not prioritised those fintech-adjacent features. What you do get is a stable, fast-loading app that rarely has outages.

The telephone contact centre is the genuine differentiator. It operates 24 hours a day, seven days a week, 365 days a year, staffed by UK-based advisers. Call wait times are generally short, a point that Which? and similar consumer bodies have noted repeatedly in their annual banking satisfaction surveys. In our test, a call at an off-peak weekday morning connected to an adviser in under 30 seconds. Complex queries about mortgage rates, switch incentive eligibility, and overdraft restructuring were handled in a single call without being transferred to multiple departments. That is not the norm for high-street banks.

Secure in-app messaging is available as an alternative to the phone. Email is not a supported contact method, which can frustrate customers who prefer an asynchronous written record. Social media support via X (formerly Twitter) is active during business hours. Overall, the service model assumes you want to speak to a person when something goes wrong; if you prefer fully self-serve resolution of every issue, first direct is less well suited than a purely app-native bank.

Reputation and real customer experience

first direct consistently performs at or near the top of UK retail banking satisfaction surveys. The Financial Conduct Authority publishes biannual service quality rankings for personal current accounts, and first direct has appeared in the top positions across multiple consecutive reporting periods. That record is worth examining for recurring themes rather than simply accepting the headline position.

The praise that appears most frequently in customer reviews centres on telephone service: short wait times, agents who listen rather than follow scripts, and problems resolved on first contact. Customers who have dealt with fraud, bereavement administration, or complex account changes report notably better experiences with first direct than with most large banks. A secondary recurring positive is the Regular Saver rate: customers who commit to monthly deposits into the linked savings account consistently highlight the competitive return compared with what their previous bank offered.

Complaints, when they do appear, cluster around a few specific areas. The online banking interface, particularly the browser-based version, draws criticism for feeling dated compared with fintech competitors. Some customers report that the switch incentive conditions are stricter in practice than they expected, particularly around the timing of qualifying debit card transactions within the required window. A smaller but persistent thread of complaints relates to the credit check at application: customers with non-standard credit histories or recent address changes sometimes find the outcome surprising given that they have managed money responsibly elsewhere. first direct does not offer a pre-eligibility soft check tool, which means a declined application leaves a hard credit search on the applicant’s file.

Safety and deposit protection

first direct is authorised by the Prudential Regulation Authority and regulated by both the PRA and the Financial Conduct Authority. As a UK-regulated deposit-taker, it is covered by the Financial Services Compensation Scheme. FSCS protection covers eligible deposits up to £85,000 per person per banking group. first direct is part of the HSBC UK group; customers who also hold deposits with HSBC UK directly should be aware that the £85,000 limit applies to the total held across both institutions combined, not separately per brand. This is a meaningful planning consideration for anyone holding large cash balances across both.

The £85,000 limit rises temporarily to £1,000,000 for certain life events: proceeds from a property sale, redundancy payments, personal injury compensation, or inheritance. This Temporary High Balance protection lasts for six months from the date of deposit and is automatic rather than requiring separate registration. For everyday customers with balances well below £85,000, FSCS coverage is sufficient and the institution itself carries the strength of one of the largest banking groups in the world.

Verdict: open it or not?

first direct 1st Account earns its strong reputation through consistent execution of a simple promise: treat customers like adults, answer the phone promptly, and do not complicate the pricing. For employed professionals who can comfortably meet the £1,000 monthly deposit threshold, the effective cost is zero and the linked Regular Saver adds genuine value that a purely transactional bank cannot match.

The account is not right for everyone. Frequent travellers who want ATM withdrawals abroad at no cost should use a dedicated travel account alongside it. People who want their current account balance to earn interest should look at providers that offer in-credit rates. Those who want deep spending analytics and gamified saving features will find the app underwhelming next to Monzo or Starling. And anyone whose monthly income is irregular or below £1,000 faces a £10 monthly fee that erodes the value proposition quickly.

If you want one bank that you can call at midnight and reach a human being who knows the product, first direct is hard to beat in the UK market. That alone justifies consideration from anyone frustrated by the automated telephone systems that dominate the rest of the high street.

How safe is first direct 1st Account?

first direct 1st Account vs alternatives

A direct comparison of the key conditions against the strongest competitors in the market.

first direct 1st AccountReviewed first direct 1st AccountReviewed | Monzo Current Account | Starling Current Account | Chase Current Account | |

| Rating | 4.0 /5 | 5.0 /5 | 5.0 /5 | 5.0 /5 |

| Monthly fee | £0/month (with monthly deposits >= £1,000; otherwise £10/month) | £0/month | £0/month | £0/month |

| Debit card | ✓ | ✓ | ✓ | ✓ |

| Credit card | ✗ | ✗ | ✗ | ✗ |

| Apple Pay | ✓ | ✓ | ✓ | ✓ |

| Google Pay | ✓ | ✓ | ✓ | ✓ |

| Cash withdrawal abroad | Free (no first direct foreign currency fee; £1.50 ATM fee may apply) | Free up to £400/30 days; then 3% (outside EEA) | Free (no Starling fees) | Free up to £500/month; then 1.5% |

| Online account opening | ✓ | ✓ | ✓ | ✓ |

| Deposit protection | 85.000 | 85.000 | 85.000 | 85.000 |

| iOS app | ✓ | ✓ | ✓ | ✓ |

| Branches | Nein (Phone & App-Banking; HSBC-Filialen fuer cash) | ✗ | ✗ | ✗ |

How we rate

About the author

Frequently asked questions

The monthly account fee is £0/month (with monthly deposits >= £1,000; otherwise £10/month).

The account is open to UK residents aged 16 and over who have not previously held a first direct account and do not currently hold an HSBC current account. Applications are completed online or by phone, and most decisions are made automatically within minutes.

There is no monthly fee as long as you pay in at least £1,000 per calendar month. If deposits fall below that threshold in any month, a £10 fee applies. There are no charges for standard Faster Payments or for paying by card overseas with first direct itself.

first direct is part of HSBC UK Bank plc, so deposits are covered by the FSCS up to £85,000 per person per bank. If you also hold money with HSBC directly, the £85,000 limit is shared across both brands rather than applying separately to each.

You apply fully online or by phone. The process uses automated identity and credit checks, so no documents need to be posted in most cases. If you want to switch from another bank, the Current Account Switch Service handles the transfer of direct debits and standing orders within seven working days.

first direct is authorised and regulated by the FCA and PRA, two of the UK's main financial regulators. The app supports biometric login and instant card freezing, and the bank provides 24/7 telephone support for security concerns. FSCS deposit protection applies up to £85,000.

Interest earned on linked savings products such as the Regular Saver falls under the UK Personal Savings Allowance. Basic-rate taxpayers can earn up to £1,000 in savings interest per tax year free of income tax; higher-rate taxpayers have a £500 allowance. Interest above these thresholds is taxed at your marginal income tax rate.