Monzo Savings Account Review 2026: Pots, ISA & Rates

Last updated: 05.07.2026

Contents

Summary

Monzo does not offer a traditional standalone savings account. Instead it built saving into the free current account app through Instant Access and Select Access Savings Pots, plus a Cash ISA, paying between 2.75% and 3.65% AER variable depending on your plan. This guide covers every Monzo savings option, what each one actually pays in 2026, and how they compare with dedicated savings providers.

Pros

- Three savings products in one app: Instant Access Pots, Select Access Pots and a Cash ISA

- Up to 3.65% AER variable on Select Access for Perks and Max subscribers

- No minimum deposit, with balances up to £1,000,000 per pot

- Interest paid monthly rather than annually

- FSCS protection up to £120,000 per person via Monzo's partner banks

Cons

- Highest rates require a paid Perks (£7/month) or Max (£17/month) subscription

- Select Access limits withdrawals to two per year before the rate drops

- Free-tier Instant Access rate of 2.75% AER trails top independent easy-access accounts

- No branch network, account management is app-only

Key facts

| Interest on savings account | ca. 2.75% AER instant access (free account); up to 3.25% AER with Perks/Max subscription |

| Deposit protection | 120.000 |

| Online account opening | ✓ |

| Welcome bonus | – |

| Joint account | – |

| Overdraft interest rate | – |

| Savings account | – |

| Rating | 4.0 /5 |

Interest rate comparison

The effective annual rate compared directly with the alternatives.

A closer look

Does Monzo actually have a savings account?

Not in the traditional sense. Monzo does not offer a separate, standalone savings account the way a building society or a challenger bank like Chase might. Instead, savings live inside the free Monzo personal current account as “Pots” — ring-fenced sections of your balance that earn interest while staying visible and accessible in the same app you already use for everyday spending. On top of Pots, Monzo also runs a Cash ISA product for savers who want to shelter interest from tax.

That structure matters for anyone searching for a “Monzo savings account”, because the answer is not one product but three: Instant Access Savings Pots, Select Access Savings Pots, and Cash ISAs (both Instant and Select Access variants). Each pays a different rate depending on how quickly you might need the money and whether you subscribe to a paid Monzo plan. This guide walks through all of them, what they actually pay in 2026, and where Monzo sits against dedicated savings providers.

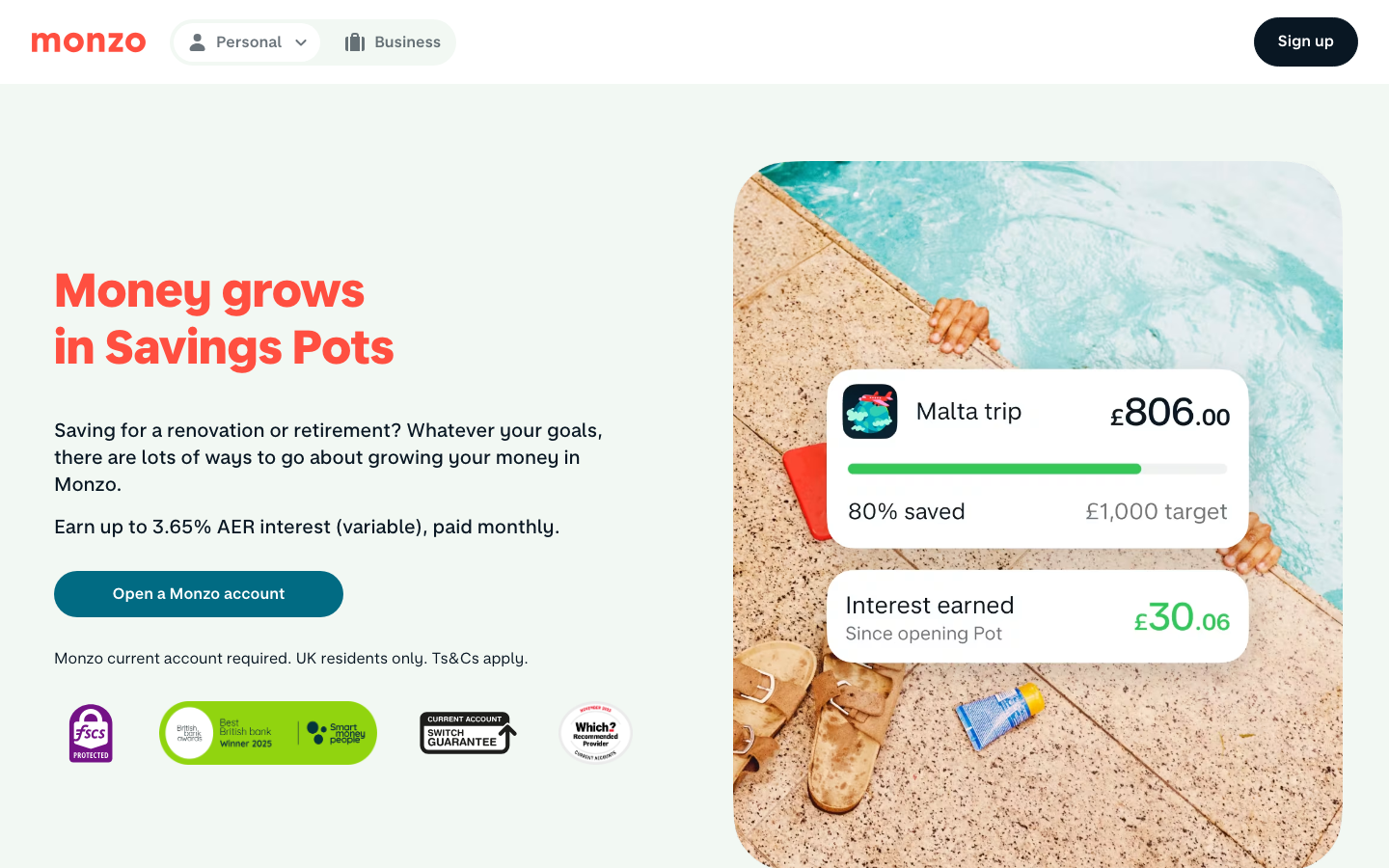

Instant Access Savings Pots: the free option

Instant Access Savings Pots are the default. Anyone with a Monzo current account can open one in seconds from the home screen, move money in from their main balance, and take it out again whenever they like, with withdrawals landing back in the current account instantly.

The standard rate is 2.75% AER variable, available to everyone on a free Monzo account. Subscribers to Monzo Perks (£7 a month) or Monzo Max (£17 a month) earn a boosted 3.25% AER variable on the same product, with a limit of £1,000,000 per Pot. Interest is calculated daily and paid out on the first of each month, rather than accruing until the account closes, which is a genuine convenience if you want to see a return build up in something close to real time.

There is no minimum deposit and no notice period. That flexibility is the trade-off for a rate that, on the free tier, sits behind the best specialist easy-access accounts currently available in the UK market.

Select Access Savings Pots: higher rates with a catch

Select Access is Monzo’s higher-paying tier, and it is easy to miss if you only look at the headline “Monzo savings account” rate. Free and Extra account holders earn 3.15% AER variable here, while Perks and Max subscribers earn up to 3.65% AER variable, again capped at £1,000,000 per Pot.

The catch is withdrawals. Select Access allows two withdrawals per Pot each year at the advertised rate. Make a third withdrawal from the same Pot, and its rate drops for the rest of that year to 2.60% AER variable on free accounts or 3.10% AER variable for Perks, Max, Plus and Premium customers, before resetting. For savers who genuinely intend to leave money untouched, Select Access pays meaningfully more than Instant Access for the same underlying safety and flexibility. For anyone who dips into savings regularly, Instant Access is the safer choice to avoid an accidental rate cut.

Monzo Cash ISA: sheltering interest from tax

Monzo also offers Instant Access and Select Access Cash ISAs, mirroring the Pots structure but with interest paid tax-free rather than counting toward your Personal Savings Allowance. The Instant Access Cash ISA pays between 2.75% and 3.25% AER variable depending on your plan, while the Select Access Cash ISA pays up to 3.65% AER variable under the same two-withdrawals-a-year rule that applies to Select Access Pots.

For higher-rate or additional-rate taxpayers, or anyone with savings large enough to exceed their Personal Savings Allowance, the ISA route is usually worth prioritising over an equivalent standard Pot paying the same headline rate, simply because none of the interest is taxable. You can hold both a Monzo Pot and a Monzo ISA at the same time, and money can be moved between them within the app.

Is Monzo Perks or Max worth it just for the savings boost?

Run the numbers before upgrading purely for interest. Perks costs £84 a year and adds 0.50 percentage points to both the Instant Access and Select Access rates. That extra 0.50% only outweighs the subscription fee once your savings balance passes roughly £16,800 — below that, the fee costs more than the rate boost earns you. Max, at £17 a month (£204 a year), needs a balance north of £40,000 in savings alone before the same logic pays off.

In practice, most people who upgrade to Perks or Max are paying for the bundled extras (a monthly Vue cinema ticket, an annual Railcard, Uber One, and other perks) as much as the savings rate, so it is worth totalling the full package rather than judging the subscription on interest alone. Savers with balances well under £16,800 are usually better off on the free plan’s 2.75% to 3.15% AER and looking at a specialist easy-access account for anything they do not need Monzo’s app convenience for.

How Monzo compares with other UK savings options

Against dedicated savings-focused providers, Monzo’s free-tier rates are respectable but not table-topping. Zopa Smart Saver and Starling Savings Spaces both compete in the same easy-access bracket without requiring a paid subscription to reach their best rates, and both are worth checking before committing significant balances to a Monzo Pot on the free plan. Revolut’s savings product follows a similar tiered-by-subscription model to Monzo, so the comparison there comes down to which app’s non-savings features you value more.

Where Monzo has a real edge is convenience: no separate account to open, no separate app to check, and interest visible next to your spending in real time. If you already bank with Monzo day to day, opening a Pot takes under a minute and costs nothing on the free plan. If you are choosing a home for savings from scratch with no existing loyalty to any provider, it is worth comparing Monzo’s Select Access rate against the top standalone easy-access accounts before deciding.

Safety: FSCS protection on Monzo savings

Monzo Bank Ltd is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the PRA. Balances held in Monzo Pots and ISAs are covered by the Financial Services Compensation Scheme (FSCS) up to £120,000 per person, a figure that reflects the temporary high-balance protection scheme rather than the standard £85,000 limit, and applies via the partner banks that actually hold pooled Pot balances on Monzo’s behalf. Monzo discloses which partner bank underpins each Pot type, so it is worth checking this if you already hold savings elsewhere with the same partner bank, since FSCS limits are combined per banking licence, not per app.

Tax on Monzo savings interest

Interest earned in a standard Instant Access or Select Access Pot counts as savings income and is measured against your Personal Savings Allowance: £1,000 a year tax-free for basic-rate taxpayers, £500 for higher-rate taxpayers, and nothing for additional-rate taxpayers. Monzo reports interest paid to HMRC, and any tax owed above your allowance is usually collected automatically through a PAYE tax code adjustment. Interest earned inside a Monzo Cash ISA is entirely tax-free regardless of your income tax band, which is the main reason to prefer the ISA once your balance is large enough to risk breaching your allowance.

How to open a Monzo savings Pot or ISA

You need a Monzo personal current account first. New customers apply through the Monzo app, complete a photo ID and selfie check, and can usually be up and running within a few minutes. Existing customers simply tap “Add pot” from the home screen, choose Instant Access, Select Access, or a Cash ISA, name the Pot, and transfer money in from their main balance. There is no minimum opening deposit on any of the products, and you can hold multiple Pots at once for different goals, each earning interest independently.

Verdict: who should use Monzo for savings

Monzo’s savings account setup works best for existing Monzo current account customers who want a simple, no-fee place to earn a reasonable rate without opening anything new. The free-tier rates of 2.75% to 3.15% AER are solid rather than market-leading, but Select Access at up to 3.65% AER for Perks and Max subscribers is genuinely competitive, provided you can live with the two-withdrawals-a-year limit.

If you have no existing relationship with Monzo and are shopping purely for the highest savings rate, compare Select Access against the top standalone easy-access accounts before committing, since specialist providers occasionally edge ahead. But for anyone who already banks with Monzo and wants savings, an ISA, and spending in one screen, the full range of Pots covers most needs without extra admin.

How safe is Monzo Savings Pots?

Monzo Savings Pots vs alternatives

A direct comparison of the key conditions against the strongest competitors in the market.

Monzo Savings PotsReviewed Monzo Savings PotsReviewed | Zopa Smart Saver | Starling Savings Spaces | Revolut Savings | |

| Rating | 4.0 /5 | 4.0 /5 | 3.0 /5 | 3.0 /5 |

| Interest on savings account | ca. 2.75% AER instant access (free account); up to 3.25% AER with Perks/Max subscription | ca. 3.25% AER easy access (Access Pots, variable) | ca. 2.50% AER easy access (Easy Saver, variable) | ca. 2.90% AER (Standard plan) to 4.00% AER (Ultra plan); Promo Boost: 5.00% AER until Dec 2026 for new customers |

| Deposit protection | 120.000 | 120.000 | 120.000 | 120.000 |

| Online account opening | ✓ | ✓ | ✓ | ✓ |

| Welcome bonus | – | – | – | – |

| Joint account | – | – | – | – |

| Overdraft interest rate | – | – | – | – |

| Savings account | – | – | – | – |

How we rate

About the author

Frequently asked questions

The account is free with no account fees. Current rate: ca. 2.75% AER instant access (free account); up to 3.25% AER with Perks/Max subscription.

Not a standalone one. Monzo builds saving into its free current account through Instant Access and Select Access Savings Pots, plus a separate Cash ISA product. All of them sit inside the same app as your everyday spending rather than as a separate account.

Instant Access Pots let you withdraw money at any time with no restrictions, paying 2.75% AER variable (2.75% free, 3.25% with Perks or Max). Select Access Pots pay more, up to 3.65% AER variable with Perks or Max, but limit you to two withdrawals a year per Pot before the rate drops for the rest of that year.

Yes. Monzo offers an Instant Access Cash ISA paying 2.75% to 3.25% AER variable and a Select Access Cash ISA paying up to 3.65% AER variable, under the same two-withdrawal rule as the equivalent Pots. Interest in an ISA is entirely tax-free.

Only once your balance is large enough. Perks costs £84 a year for a 0.50 percentage point rate boost, which breaks even at roughly £16,800 in savings. Max costs £204 a year and needs around £40,000 to break even on the rate alone, so most subscribers are also paying for the bundled non-savings perks.

You can open multiple Pots at the same time for different goals, each earning interest independently, with a cap of £1,000,000 per Personal Instant Access or Select Access Pot.

Monzo Bank Ltd is authorised by the Prudential Regulation Authority and regulated by the FCA and PRA. Savings balances are covered by the FSCS up to £120,000 per person, applied via the partner banks that hold the underlying funds, so it is worth checking which partner bank that is if you hold savings elsewhere too.